#002: Fooled By Randomness - Nassim Taleb

Why lady Fortuna rules our lives and why you shouldn't be checking your email every minute

Too Long, Maybe I’ll Read:

Summary: Fooled By Randomness covers how uncertainty, lack of probabilistic acumen and overall human limitations hinders our capability of forecasting, thinking about the future and past and ultimately making decisions. It uncovers human flaw and lets us be better knowing that.

Why read it: to understand how much uncertainty is pervasive and invisible and how easy it is to be mistaken when dealing with matters of probability. It's an easy read with depth of concepts and stories.

What you get from it: if you're new to matters of human biases and uncertainty, this book will give you understanding of standard human limitations when making decisions. Further, it will give you many financial market examples of how we are mis-influenced, misguided and, in some cases, ruined by randomness.

Rating:

Timeless? ⚠️ It's recent - 2001

Comprehensive? ✅ cases are solid for the theses presented

Mental model? ✅ it includes many ideas that add to your mental models

Return on investment of reading? ✅ easy to read book

One-sided VS full-scoped? ⛔️ the author has a clear and divise opinion

All in all: ⭐️⭐️⭐️⭐️(4/5)

Should you read it? 👍I found it to be a good return on investment. Easy and entertaining to read, interesting fictional stories, solid ideas rooted in Taleb's experience as a trader, educational and connected with scientific foundations.

Before we start:

I’m reading 100 books like this one and will be sending you summaries so you can decide if you want to read it yourself. If this is interesting, consider subscribing below

The book

Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets

By Nassim Nicholas Taleb (website)

Summary

First and foremost, doing a summary of this book is self-defeating. Taleb believes a book should be self-standing that you cannot reduce, otherwise you'd just read the summary. This is clear as soon as you start reading the book. Fooled by Randomness is weaved with fictional stories, finance anecdotes, probability concepts and the author's own opinion. It’s hard to break apart this fabric.

But try we must. Let’s jump into my selection of key topics.

We confuse luck with skill - and there's no easy way to solve this

We're very easy to attribute to skill what is due to luck. Our actions are not (necessarily) cause for success.

The book starts by telling the story of Croesus, an exuberant king, who was visited by Solon, a wise greek legislator. After failing to impress Solon, Croesus asked directly if he was not the happiest person Solon had ever seen. Solon replied:

“The observation of the numerous misfortunes that attend all conditions forbids us to grow insolent upon our present enjoyments, or to admire a man’s happiness that may yet, in course of time, suffer change. For the uncertain future has yet to come, with all variety of future; and him only to whom the divinity has [guaranteed] continued happiness until the end we may call happy.”

Years passed and life changed for Croesus when he is captured, sentenced to burn at the stake by King Cyrus. Ultimately King Cyrus saved Croesus when he heard his screams for Solon’s name and heard Solon’s warning, ultimately fearing the same fate as Croesus’.

Beyond the platitude of ‘Wealth not meaning happiness’, the moral of the story pertaining to this book is: that which came with the help of luck could be taken away by luck.

This becomes a central thesis of the book. That luck is behind wins and losses. That people will tend to see success as a result of skill and failure as a result of bad luck. That everything that came from luck can easily be destroyed by luck as well. The opposite is true: that which had little luck involved is more resistant to luck.

To take this concept further, Taleb describes:

Mild success can be explainable by skills and labor.

Wild success is attributable to variance.

So the more outlandish and exuberant the success the more likely it is that it’s due to randomness.

Taleb tells the story of Nero, the hero of the book and a trader who was fascinated with risk and uncertainty and always took de-risked positions. Jack, his neighbor also a trader, had more success financially as he took more aggressive and riskier bets. This frustrated Nero. After a while, Jack is fired due to risk finally catching up to him and Nero thinks the world is finally balanced.

This idea of risk finally catching up with someone is called Ergodicity. Ergodicity in probability means that, given very large sample paths (i.e. scenarios or different possibilities) and enough time, these paths end up resembling each other. In other words, time eliminates the effects of randomness.

So randomness is everywhere, invisible and misleading to us. And greatly affects our decision making.

Let’s look into how randomness affects decision making.

Decisions and outcomes are two different things

Another consequence of luck having a larger role in our everyday decision making is understanding that as soon as we pull the trigger on a decision, we will need to leave space for luck. This is why it’s important to decouple the quality of decisions from outcomes. We can't measure performance of a decision based on the outcome but by the cost of the alternative. Taleb says:

A mistake is not something to be determined after the fact, but in the light of the information until that point.

We look to history to honor this idea and how we think of people as ‘Heroes’. Heroes exist regardless of winning or losing wars. They exist because of their heroic behavior. In Portugal, a hero by the name of Martim Moniz is celebrated. According to the legend..

Martim Moniz was a knight participating in the Christian invasion force, led by king Afonso I of Portugal, in the Siege of Lisbon, during the Reconquest. At one point in the siege of São Jorge Castle, he saw the Moors closing the castle doors. He led an attack on the doors, and sacrificed himself by lodging his own body in the doorway, preventing the defenders from fully closing the door. This heroic act allowed time for his fellow soldiers to arrive and secure the door, leading to the eventual capture of the castle. Martim Moniz was killed in the incident. In his honor, the entrance was dubbed Porta de Martim Moniz (Gate of Martim Moniz).

The quality of the Moniz’s decision had him killed, which by all measures is not really positive. But we evaluate the bravery of his decision. And although ultimately we look back to think that it was crucial to capture the castle, he didn’t know that would be the result. And we celebrate that moment.

On this topic, Taleb mentions several times Pascal's wager, which explores the outcomes of believing or not in God. Ultimately, it proposes a utilitarian view into decision making given that believing in God would mean infinite gain and not believing in God would be infinite loss:

This means that even if one doesn't believe in god, the alternative is infinitely worse. Then for practical matters, it’s only logical to believe. What it means is that there are decisions where the upside is limited but the downside is catastrophic. We should try to map as much as we can potential outcomes knowing that predicting said outcomes is many times impossible.

Noise causes unhappiness and stress

Using his trusted Monte Carlos setup, Taleb creates a scenario where he assumes an investment with 15% return and 10% margin of error

At the end of the year, there's 93% probability of success for this return. But as we shorten the time frame, the probability of success will get lower and lower until we get 50% on a second basis. The same as flipping a coin.

So the investor that looks at her phone to check the performance of her investment will suffer on a minute by minute basis with the ups and downs. Imagine now that this investor would get a report every month, which would mean 67% probability. The agony of seeing ups and downs would be replaced by some comfort in her original investment decision.

Our brains and emotions are not designed to be flooded by information every second. People who look too frequently at news or data burn out. This is because negative news outweigh positive news even if they are the same number. This same idea could easily be applied to looking every minute to Slack or E-mail.

This is why you should review your level of information accordingly. New things created by technology have created the idea that new is always better. This does not apply to information. New things are in great volume and require effort in filtering to find quality. Time is the greatest filter since something that is relevant today, and has been for a long time, will likely continue to be relevant (called the Lindy effect which Taleb explores further in Black Swan and Anti-fragile). This is also to do with the opportunity cost of this filtering - you could be reading or watching something amazing, and proven by time, instead of filtering mediocre content.

This is specially problematic when dealing with journalistic news as it can fill our minds with anxiety and emotion given that that's the modern journalistic incentive - to get views and clicks. People believe that the next article they read on FT will finally make everything make sense. It's a sort of a Hedonistic Treadmill.

As we are not rational and prone to randomness, our emotions take the best of us when we look at news. So in order to make good decisions and live a better life, you need to deprive yourself of noise and variance of news.

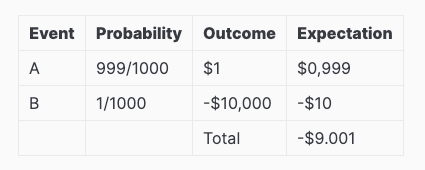

Magnitude is more important than frequency

A key concept that Taleb feels strongly is that the magnitude of the outcomes of events are at least as important to the frequency by which they occur.

Consider the following scenario which maps two events. Event A with high frequency and small win. B with low frequency and high loss .

If we calculate the expectation (Probability * Outcome), we get that adding those two would mean a net loss of -$9.001 This means that the frequency (the 999) is less important than the magnitude of the event (-$10,000).

When there are overwhelmingly positive rare event (infrequent but high positive magnitude), these are called Skewed bets which can give extraordinary outcomes. Skewed bets play on the concept of asymmetric odds and outcomes.

Our school system has taught us to ignore rare events and to focus on averages. This is a mistake. Many scientists for years would remove maximum world temperatures to not skew averages. For this reason, these scientists failed to see a pattern of global warming in the early days.

Non Linearity - or why it feels like forever to get good at something

Non linear dynamics are seemingly disproportionate event/outcomes from seemingly small accumulating (linear) actions. Like building a sand castle, one grain of sand (linear action) will be too much and will make the construction topple (non linear outcome). It's also known as Chaos Theory.

Learning is non-linear because you don't understand how much you're learning over time. You take lessons every day and it feels frustrating to not feel better. But then one day you find that all of a sudden everything clicks and you’re much better than before.

Our brains have a hard time understanding non-linearities as they are programmed to think cause ⇒ effect.

Human Biases/Heuristics and limitations understanding Randomness

It's hard to understand randomness. As such, we try to see correlation and causality where many times there is none.

In logic there is Deduction, where we infer the instance based on a rule, and Induction, where we infer a rule based on instances. Our brains love induction and are very much attracted to seeing rules everywhere, given that we have an easier time remembering if there is causality between events (instead of remembering every single event, we remember only the rule). This makes us see causality in places where there might not be causality. This is because it's more efficient when we make decisions. Herbert Simon said that if we were to optimize every decision we make, we would need infinite time and energy.

When stocks are high 1% people might want to see reason for that to happen (in case of financial journalists, they are paid to do so), however it's variance. If I run a 10k bicycle race and I win by less than 1 sec, I can't say that I'm better than my opponent.

B.F. Skinner found that, when feeding pigeons and rats at random, animals would develop rituals and ceremonies which they thought would make food appear (like rain dancing).

The brain is a machine for jumping to conclusions

Kahneman, Tversky

The scientific community of behavioral psychologists agrees on this:

We do not think when we make choices, instead we use heuristics which are efficient quick ways to optimize decisions (or biases).

We make serious probabilistic mistakes in Today's world

What we call Heuristics, named by Kahneman and Tversky, are really human ingrained shortcuts to make decisions which we normally call Biases.

Let’s discuss a few ones from the book.

Survivorship bias

The highest performing realization will be the most visible. And losers don't show up.

When a scientist was asked to make sure how to reinforce RAF fighter planes in world war II, the immediate reaction was to count the number of bullet holes in order to introduce steel plates in those areas. However, what he did was actually reinforce the parts of the planes that didn't have any bullet holes, as he inferred that planes with bullet holes in those sections did not show up. In other words, the scientist saw beyond the survivors and understood why losers did not show up.

Survivor bias is the intrinsic desire to focus our attention on the winners and forgetting that there are losers.

Imagine you got rich and moved into an ultra rich neighborhood. Imagine that your neighbors are richer than you. It's inevitable to feel miserable because you will be comparing yourself with winners and you won’t be able to compare yourself with the people less rich than you because they are not there. This inevitably messes with emotions.

Survivorship bias manifests itself in other forms as well. Imagine you have infinite monkeys typing at a keyboard. It becomes likely that there will be a monkey who will write the Linux Kernel. So performance, and specially analysis of historical performance, needs to take into consideration:

The randomness of the profession

How many 'monkeys' there are working (this is because, the larger the number of monkeys, the more likely there will be survivorship bias involved)

It is common that we retrofit rules to match our data. This is called Backtesting or data snooping. This allows for people, for example, to create meaningless correlations like the size of skirts to the performance of stock in a country.

In many points in life we could be playing Russian roulette unknowingly, because we're tempted by outcomes or wealth we see in other people, without knowing the blowouts of the people that lost competing for those rewards. We don't understand the risk of certain decisions but it's easy to be seduced by the payoffs we see, that have a lot of luck involved. This is to do with Survivorship Bias.

An antidote: It's very valuable to think about what doesn't work, like the scientist looking at sections of the planes without bullet holes (Markman, Linderberg, Kray)

Loss of perspective Tendency

You don't have all the knowledge present in your mind at all times, it's much easier to remember the last available fact or event. It's easier for the brain to think about delta vs absolutes. Which means that we have a harder time thinking about global instead of local events. Humans suffer because they cannot get perspective on events. Traders, for example, suffer from "You're only as good as your last trade"

This is also one of the reasons why Brainstorming doesn't work (Schacter 2001, Streck Mussweiler 97). Brainstorming is not optimal because it favors recent ideas that likely have emotions attached to them, reducing rationality. We also tend to like our first ideas the best.

For more on psychological tendencies, these are high signal resources:

The Psychology of Human Misjudgment - Charlie Munger

Thinking Fast and Slow - Daniel Kahneman

What we can do: be brave

So much of life is at the hands of luck that the ancient Romans believed in the power of the goddess Fortuna.

The ancient stoic philosophers believed in taking the dignified path when things go wrong. To get even with luck. A stoic has wisdom, upright dealing and courage. Dress your best suit for your execution. Take it in the chin. Taleb writes:

Hide your cancer from others as the dignified attitude will make defeat and victory look heroic

I’ll add to this a meditation from Marcus Aurelius:

Man can't lose any other life than the one he lives

Man can live any other life than the one he loses

Man only has the present. The past is gone and the future is up to Fortuna.

Conclusion and thoughts

This book was arguably the book that first made N.N. Taleb famous. It is the first step in the path of building the Black Swan, Anti-fragile and Skin in the Game, which made Taleb transcend mere non-fiction author to Nostradamus type of following.

A few more interesting things from reading the book:

Taleb shows a strong dislike for business bottom-line types, MBAs (despite having one).

He loves his Monte Carlo setup.

He enjoys a life with adversaries:

Life would be unbearably bland if we had no enemies on which to waste efforts and energy

He also shows strong dislike for normative economics writing:

Normative economics is like religion without the aesthetics

This has made me curious to explore his more recent literature.

Final thought: like many of the books I read, reviews and summaries will always feel like 'Pinning a Medal on Mount Everest for Being the Highest Mountain'. Regardless I hope I made a strong case for you to read this book.

Appendix

Authors, books and references

- Karl Popper

- Adam Smith

- Herbert Simon

- Daniel Kahneman and Amos Tversky

- Possible world semantics - Saul Kriple

- States of Nature - Kenneth Arrow - Scenario analysis

- Iliad - Homer

- Irrational Exuberance - Robert Schiller

- Stock prices and Social Dynamics - Robert Schiller

- Fashionable Nonsense (comedy) - Alan Sokal

- Mean Genes - Burnham

- Decartes' error- Damasio

- Emotional Brain- LeDoux

- Taleb's Google talk